HMO Mortgages: Your Guide to Smarter Property Investments

HMO mortgages are designed for landlords renting properties to multiple tenants. They provide financial solutions specifically for Houses in Multiple Occupation (HMOs). Whether you’re a seasoned investor or new to HMOs, choosing the right mortgage can help you boost rental income and manage your properties more easily.

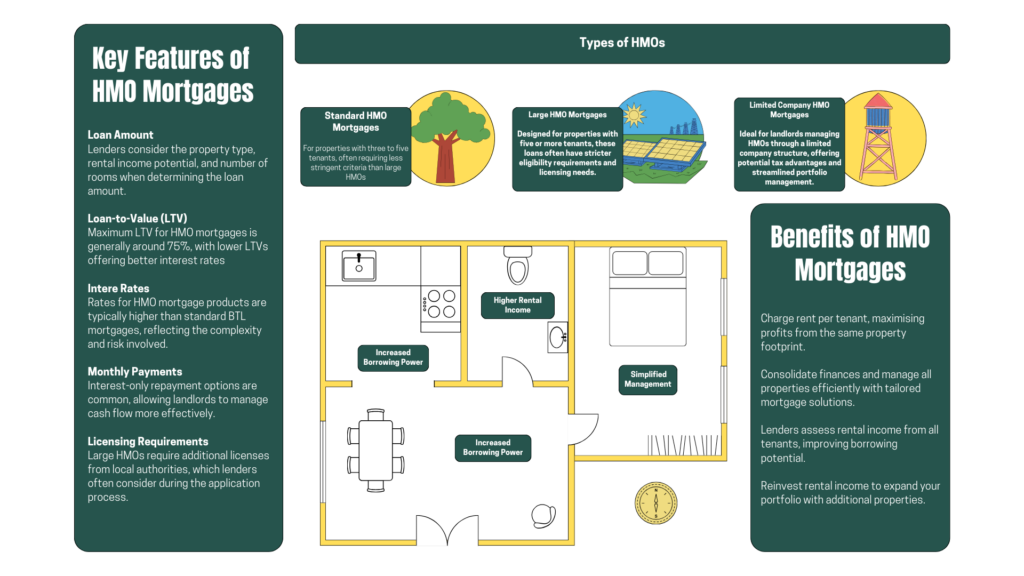

What Is an HMO Mortgage?

An HMO mortgage is a loan made for properties where tenants share facilities like kitchens or bathrooms. These mortgages are suited to landlords of HMOs, which typically offer higher rental income compared to regular buy-to-let properties.

Some larger properties, classified as large HMOs, may require additional licensing from local authorities. These properties typically house five or more tenants and must meet strict safety and compliance regulations.

Why Consider an HMO Mortgage?

Here are some reasons landlords prefer portfolio mortgages over standard buy-to-let products:

Enhanced Rental Yields

HMOs often generate significantly higher rental income than single-tenancy properties because landlords can charge rent per tenant.

Risk Management

With multiple tenants, the loss of one renter has less impact on overall rental income, reducing financial risk.

Tax Efficiency

Landlords operating through a limited company can benefit from tax advantages, such as deducting mortgage interest payments as business expenses.

Costs Associated with HMO Mortgages

- Application Fees

Lenders charge these to process your application, often 1%-10% of the loan value. - Valuation Fees

A professional valuation is required to assess the property’s worth and rental potential. - Early Repayment Charges

Exiting a mortgage deal early may incur additional costs. - Legal and Licensing Fees

Include costs for HMO licensing and ensuring the property meets legal standards.

HMO Mortgage Rates

Interest rates for HMO mortgages vary based on:

- Property Size: Larger properties often have slightly higher rates.

- Rental Yields: Higher yields may result in more favorable terms.

- LTV: Lower LTVs typically attract better rates.

Using an experienced mortgage broker can help you secure competitive HMO mortgage rates tailored to your circumstances.

Frequently Asked Questions

What is an HMO property?

An HMO is a property rented out to three or more tenants from different households who share common facilities.

Are HMO mortgage rates higher than standard buy-to-let rates?

Yes, HMO mortgage rates are typically higher due to the additional complexity and perceived risk.

Can first-time buyers apply for HMO mortgages?

A: First-time landlords may qualify, but they often need higher deposits and meet stricter lending criteria.

How does the licensing process affect HMO mortgage applications?

Properties must comply with local licensing requirements, which lenders assess before approving a mortgage.

What are the benefits of managing HMOs through a limited company?

Limited companies can offer tax advantages, such as deducting mortgage interest payments, and may simplify portfolio management.

Why Choose The Landlords Broker for HMO Mortgages?

At The Landlords Broker, we specialize in finding the best HMO mortgage solutions for landlords. Here’s how we can help:

Expert Advice

Guidance on managing HMOs, from standard properties to large, licensed setups.

Wide Lender Network

Access to lenders offering competitive rates and flexible terms.

Tailored Solutions

Options for first-time landlords, experienced investors, and limited companies.

Transparent Costs

Clear breakdowns of application fees, interest rates, and other expenses.

Get Started Today

Whether you’re investing in your first HMO property or expanding an existing portfolio, we can help. Contact The Landlords Broker today to explore HMO mortgage options tailored to your needs.